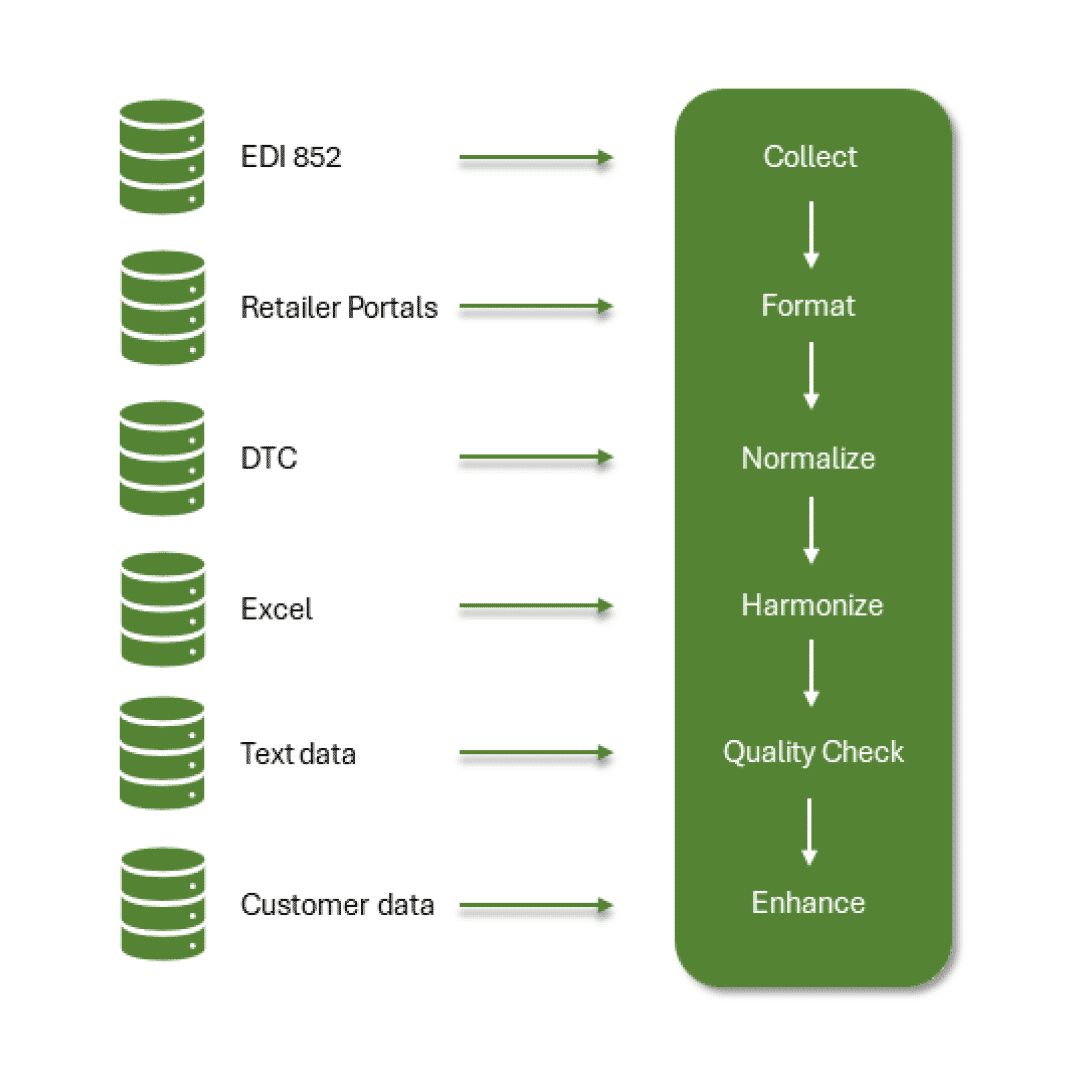

One centralized platform for all your retail data

(EDI 852, POS and DTC)

20 years of experience supporting leading beauty brands

Monday morning reports delivered

Imagine reports ready on Monday morning (or daily if you prefer) with your first cup of coffee. Unlock powerful reporting that enables you and your sales team to react in minutes, not days.

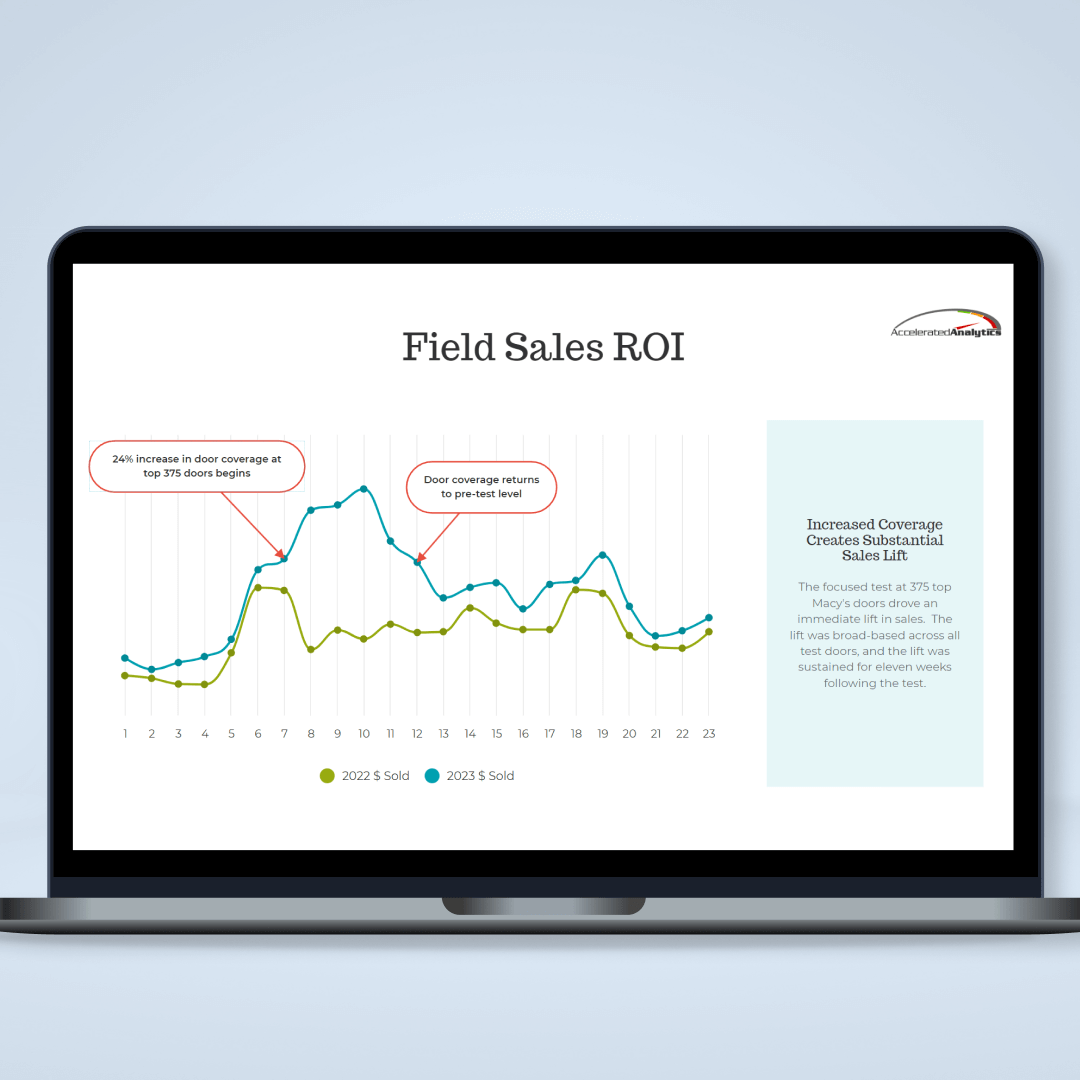

Calculate ROI on field sales and promotions

Insightful reports provide a detailed understanding of the return on investment of field sales and promotions. Our data allows sales and financial leaders to make informed decisions to drive profitable growth.

SKU and store insights

Get detailed insights on every SKU at every store. Uncover and track patterns in sales and inventory with ease. Guarantee you have the right amount of inventory, in the right locations at all times.

Less admin, more selling

Spend more time selling and less time pulling manual reports. All your retail data in one location, harmonized and ready for you to analyze. Get your team out of spreadsheets and portals, and back to selling.

Data management

Our managed data service allows you and your teams to spend more time selling. Our team will handle data collection, harmonization and report building so you can do what you do best and we will geek out on the data for you.

What do we do?

All your sales and inventory reporting one place

Collect and

Aggregate Data

We collect all your retail data (EDI 852, POS, DTC) and securely store it in our database.

Transformation

We then transform, validate, harmonize, and enrich your data with industry best-practice retail calculations.

Insightful reports

We store all your data in one central location so that you and your team can access it anywhere, any time - from the web, via email and in Excel. You choose.

Customer Success

We’re here to help you every step of the way. Each of our customers is assigned a dedicated account manager to help you get the most from the platform.